See what you can actually afford.

Banks approve you for more than you should spend. We do the math that includes your real life: income, taxes, debts, expenses, savings.

Free — no sign-up, no email.

Your numbers stay private. We never save your financial details.

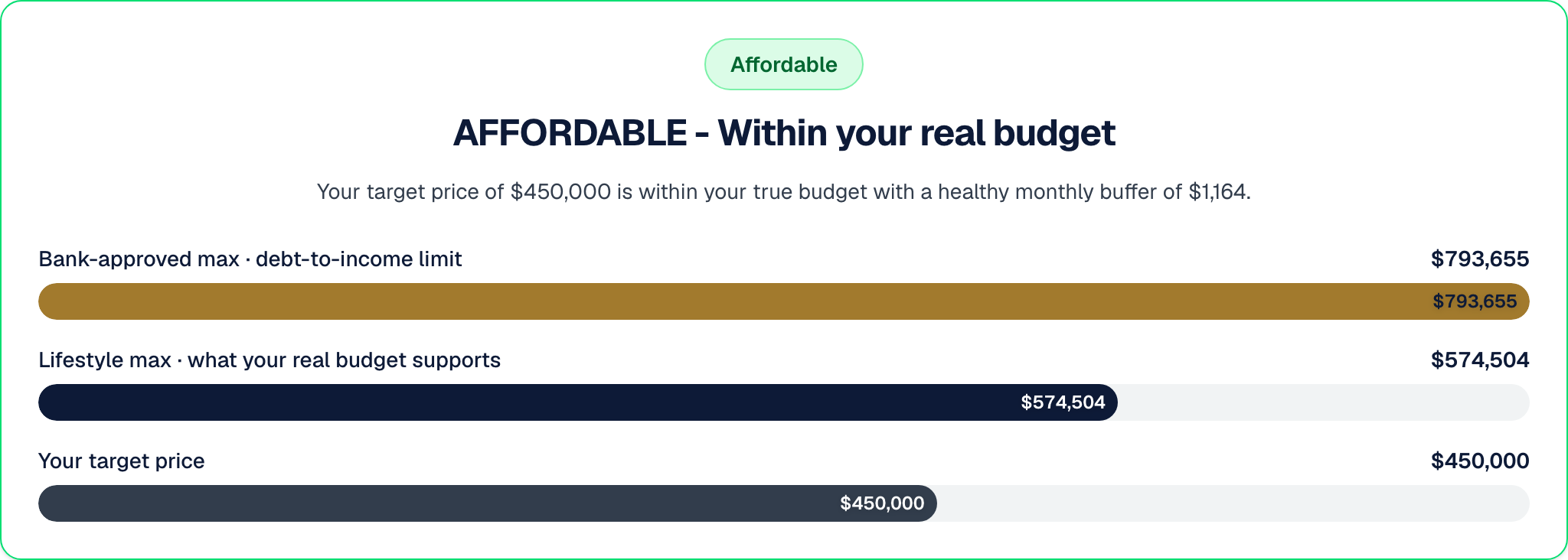

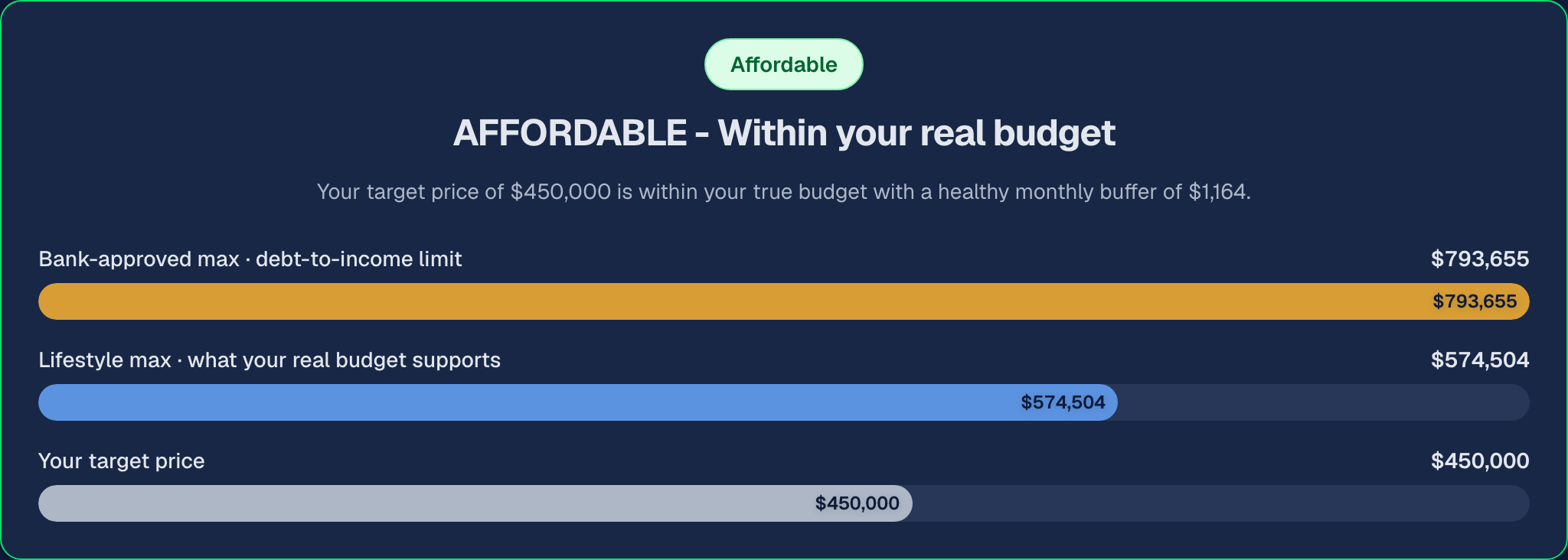

The math lenders use, plus the real-life costs they leave out.

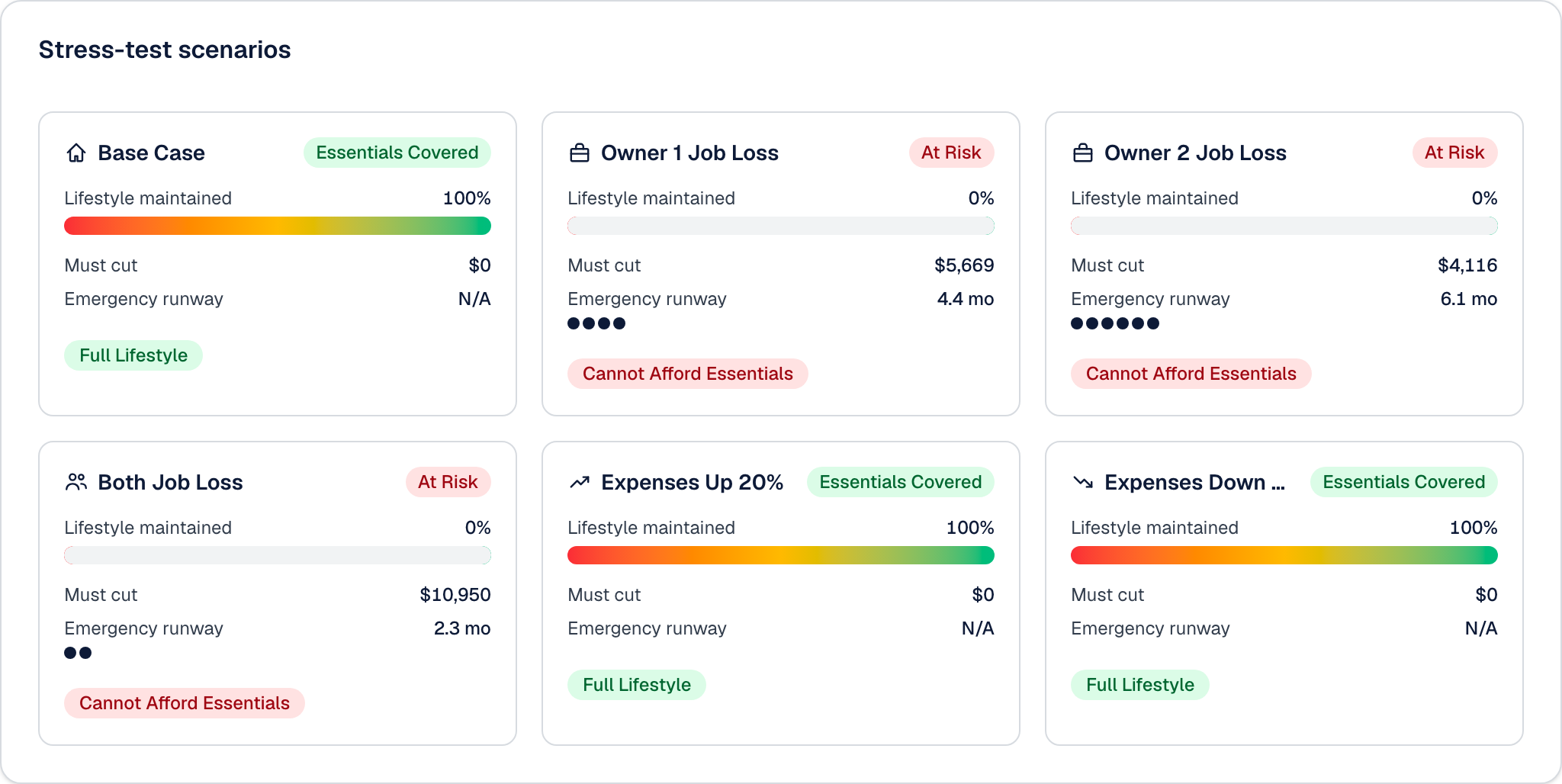

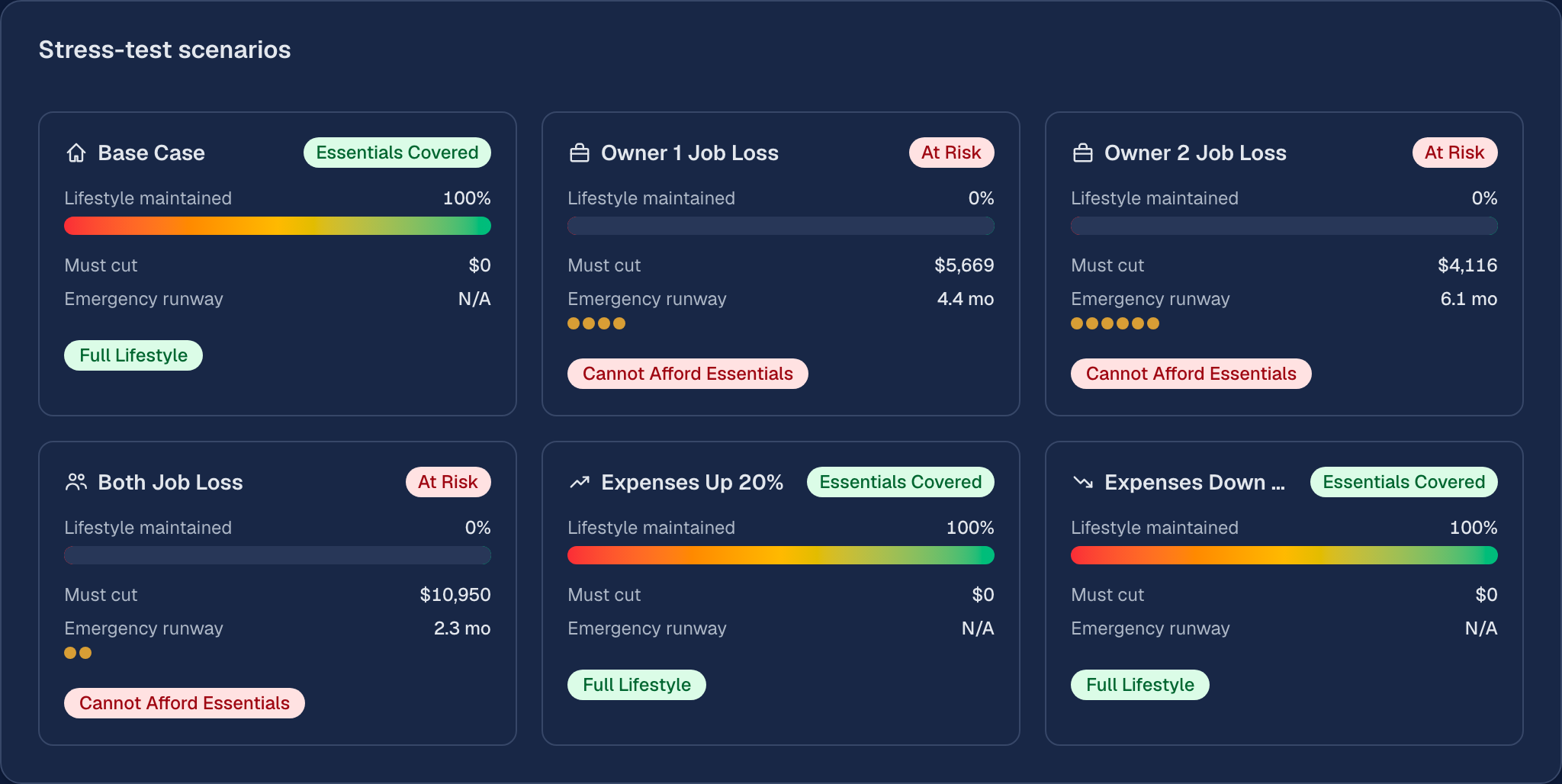

Stress-tested against multiple scenarios.

Up to six scenarios per household: job loss, expense spikes, both incomes lost. The number holds when life turns.

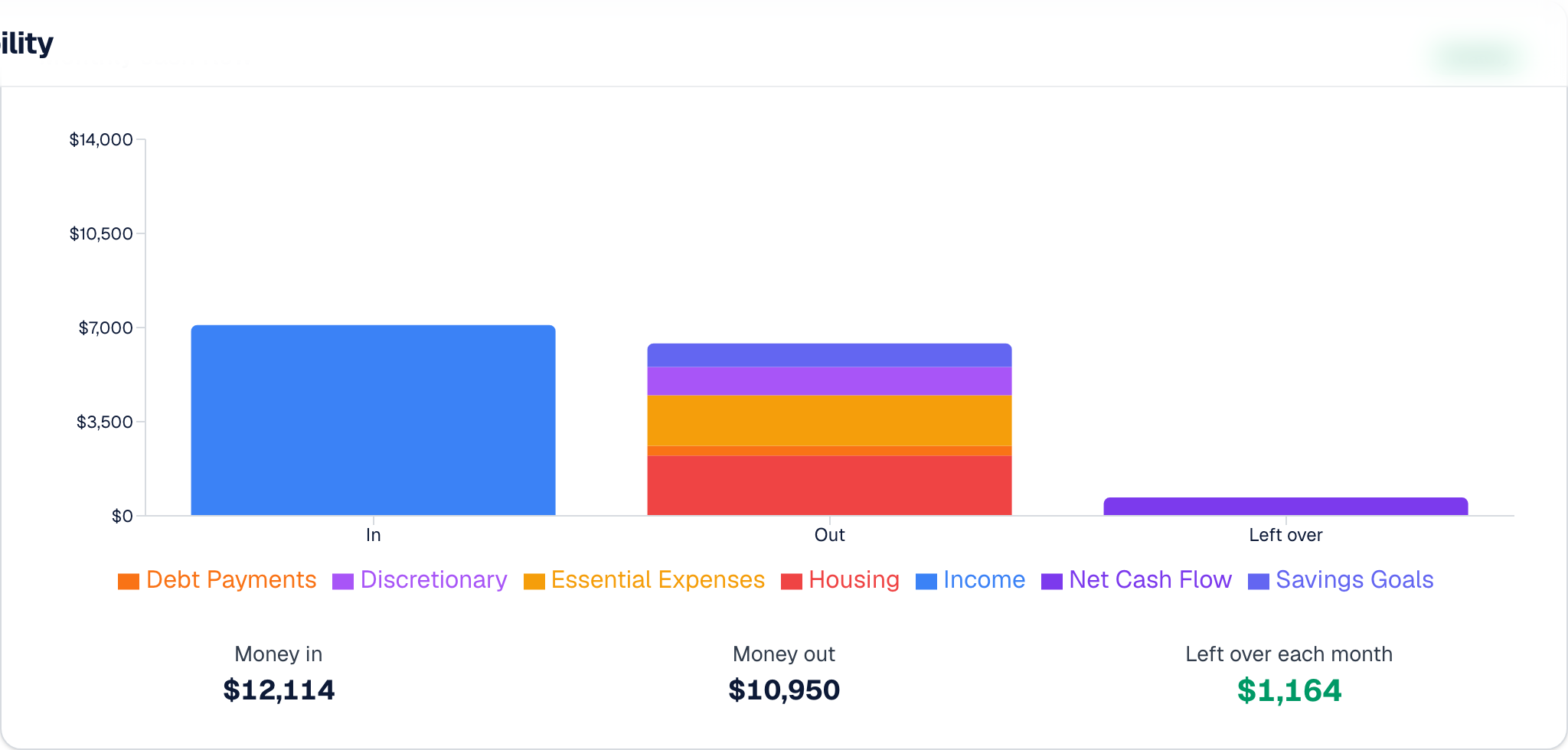

See where every dollar goes.

Watch the month resolve to what's actually available.

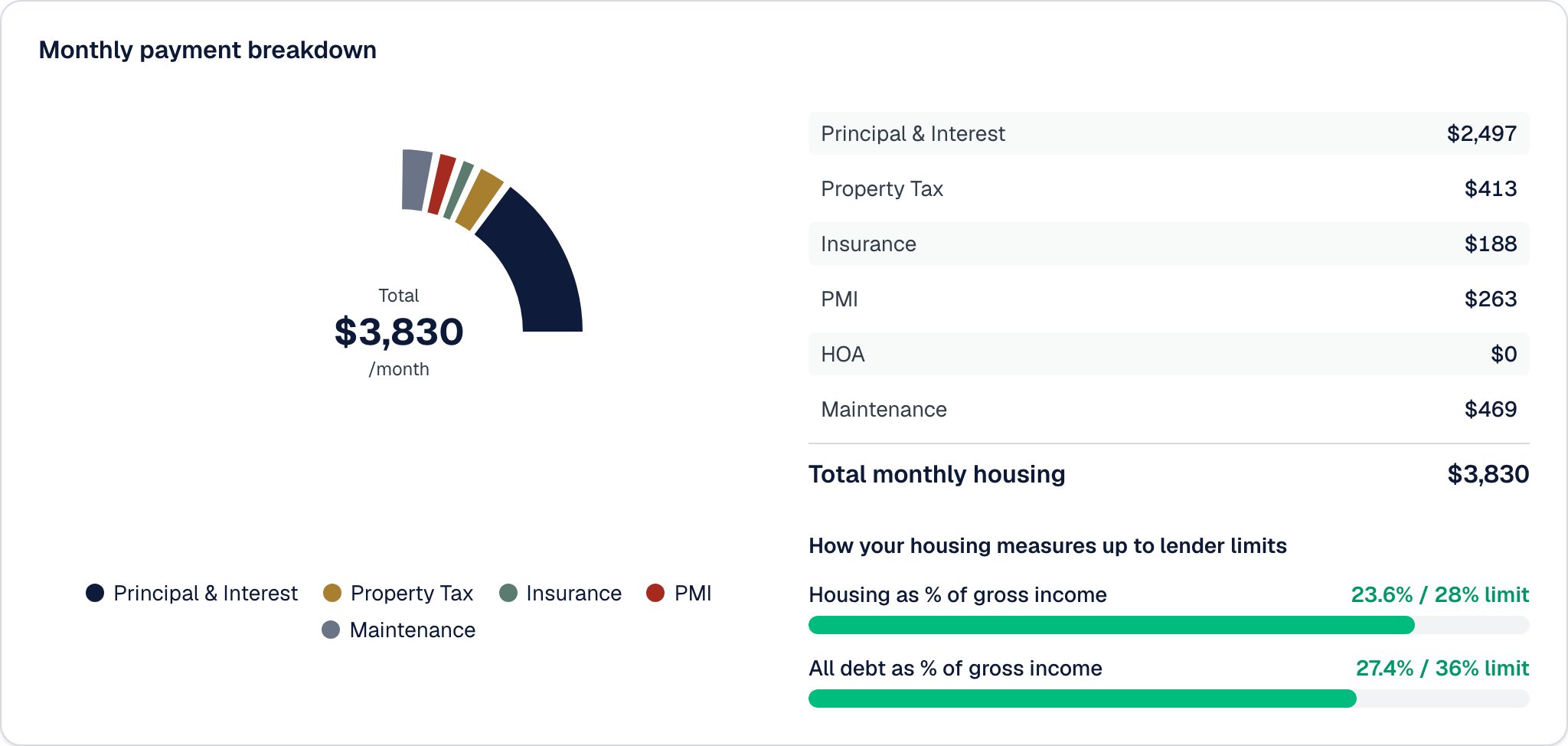

Know your real monthly payment.

The true cost of the home, not just the loan.

How it works

1

Tell us about your money.

Income, debts, monthly expenses, savings goals.

2

See your two numbers.

What the bank would approve, and what your real life supports.

3

Stress-test the year.

Job loss, expense spikes, rate changes. See how the numbers move.